Can ESG Tokenisation Resolve Income Bias in Sovereign ESG Scores.

December 10, 2025

4 Minutes

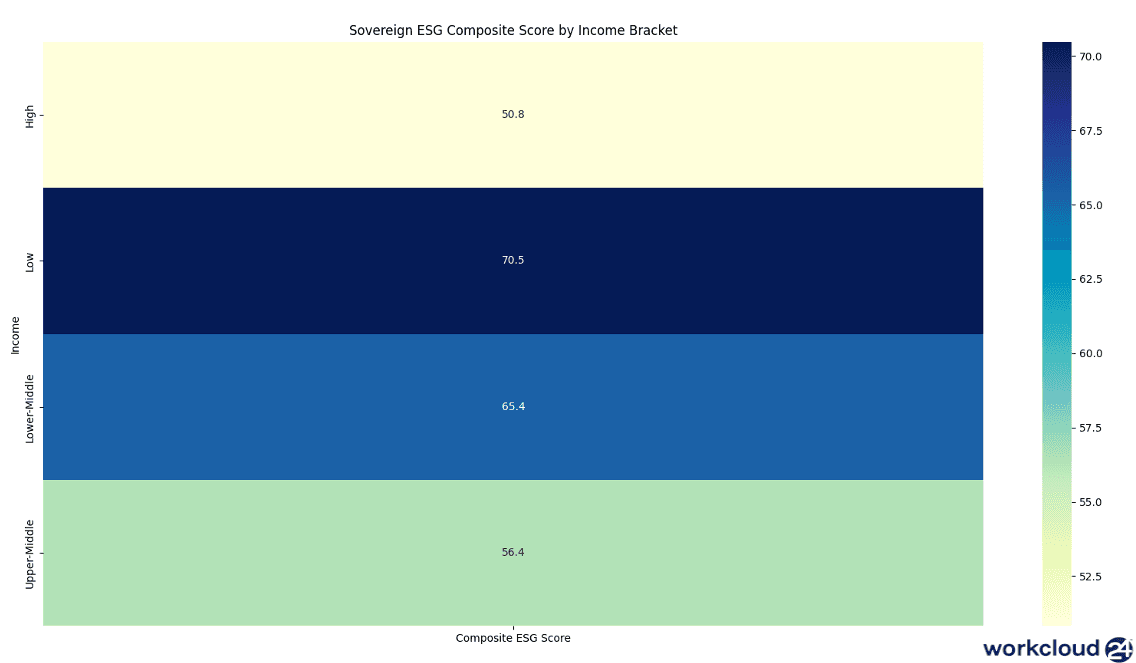

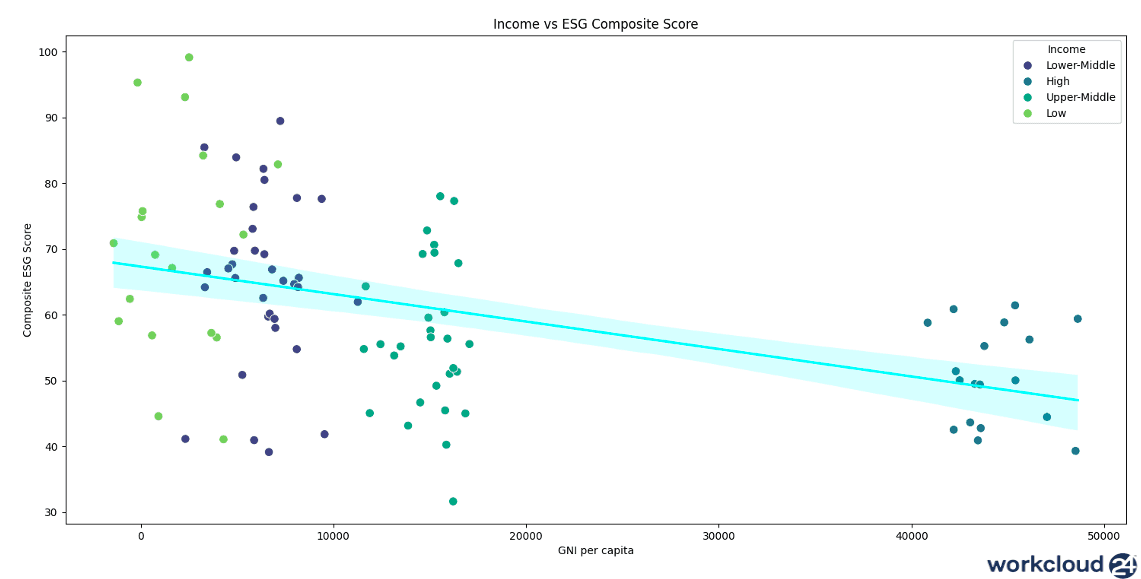

One of the biggest challenges in sovereign ESG investing is “income bias”: traditional ESG scores correlate strongly with GDP per capita, meaning high-income countries score well by default while developing economies where sustainable investment is most needed are structurally disadvantaged. This skews sovereign ESG indices and reduces capital flows to the regions that need transition funding the most.

Tokenisation provides a potential structural fix. Tokenised sovereign bonds can embed transparent, continuously updated ESG attributes and SDG indicators at a far more granular level than current scoring systems allow. Smart contracts can incorporate income-peer benchmarking, net-zero commitments, and governance progress directly into pricing logic.

ESG-Adjusted Sharpe Ratio = (Rp – Rf / σp) x (1 + (Composite ESG Score / 100))

That means countries are evaluated on sustainability momentum not their starting point. Over time, this creates a more equitable, data-rich, and performance-aligned sovereign bond market where ESG pricing reflects real progress rather than historical privilege.

Author of this Article

Hubert Abt - Founder & CEO

INSIGHTS & RESOURCES

See other interesting news

Sed ut perspiciatis unde omnis iste natus error sit voluptatem accusantium doloremque laudantium, totam rem aperiam.

Want to learn more?

Book a free consultation with Hubert!

During the call we will explain the process in details and answer any extra questions you may have