Germany’s ESG Line Shifts: Defence Enters the Portfolio Conversation

17. Januar 2026

5 Minutes

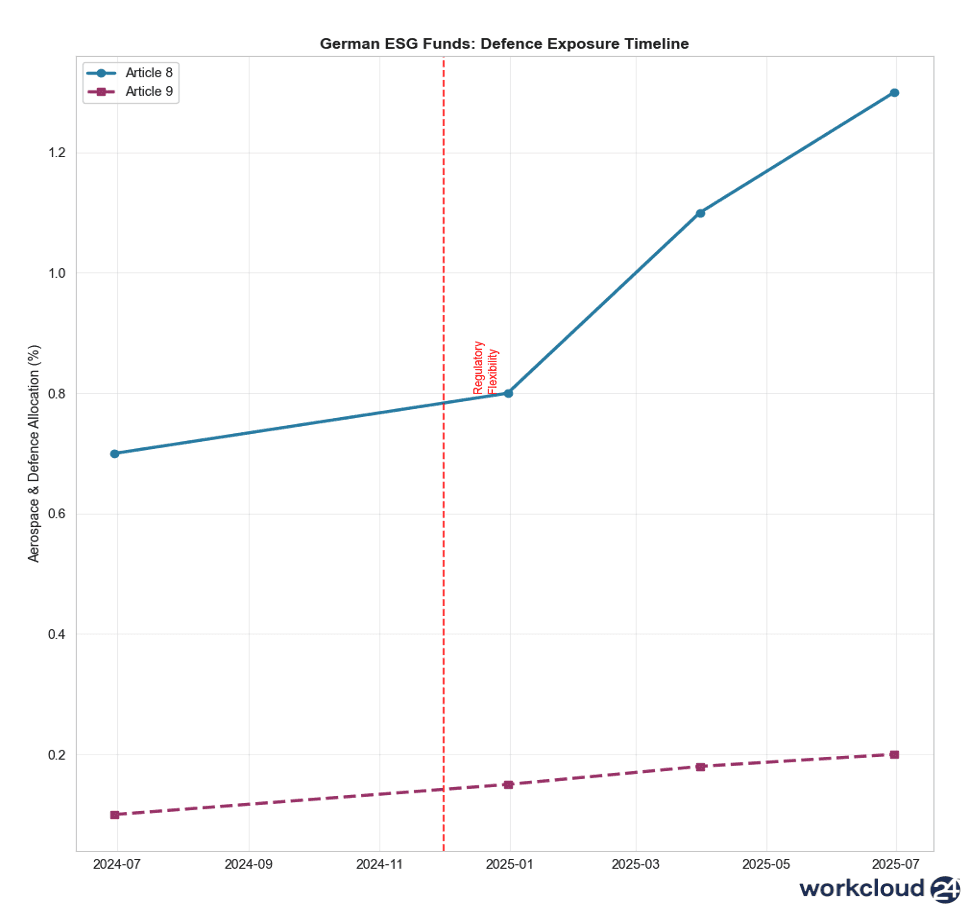

Germany’s ESG landscape is quietly but decisively changing and asset managers and investors should pay attention. Following a regulatory adjustment in late 2024, German ESG funds are no longer bound by the old 10% revenue cap on military hardware. Since December, Germany’s ESG Target Market rules only exclude weapons banned under international law. The result: defence is no longer structurally off-limits for many “sustainable” strategies.

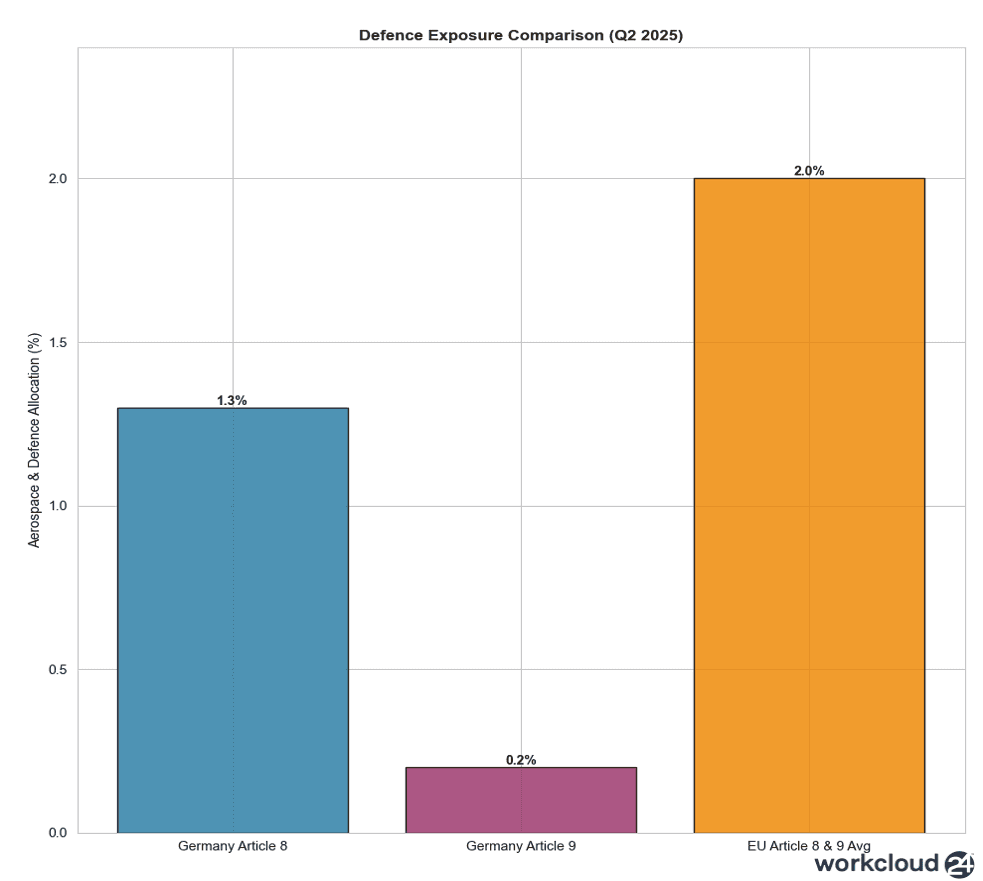

According to data from the German fund’s association BVI, managers have responded in three distinct ways. Church-affiliated and values-based investors continue to exclude defence entirely. A second group allows limited exposure where defence revenues are marginal. A third cohort has removed exclusions altogether, treating defence like any other industrial activity, subject to risk and revenue materiality. The numbers show the shift. By June 2025, aerospace and defence exposure in Article 8 funds rose from 0.8% at end-2024 to 1.3%. German-focused products stand out, with allocations reaching 4.6%, including names such as Airbus and Rheinmetall. Even Article 9 funds traditionally the most restrictive now show a measurable 0.2% exposure.

Context matters. Conventional funds still allocate more aggressively, with around 3.6% in defence, while Article 8 and 9 funds elsewhere in Europe already average close to 2% (Morningstar, Q1 2025). BVI expects German ESG allocations to continue converging toward European peers over the rest of the year. This evolution is happening alongside a notable split in capital flows. By mid-2025, German Article 8 and 9 funds oversaw more than €1.2 trillion, largely due to reclassified institutional Spezialfonds. Retail ESG assets, however, fell below €750 billion. In the first half of 2025, conventional retail funds attracted nearly €50 billions of inflows, while sustainable funds saw €1.3 billion of outflows. Institutional investors placed more than three times as much into Article 6 strategies as into Article 8 and 9 combined.

For asset and investment managers, this is less about “ESG abandoning principles” and more about ESG being redefined around security, resilience, and geopolitical reality. For real estate investors, the parallel is clear: sustainability frameworks are becoming more pragmatic, focused on transition credibility, cash-flow durability, and strategic relevance rather than rigid exclusions. Germany’s ESG market is not turning its back on sustainability. It is recalibrating it. And portfolios across equities, credit, and real assets are adjusting accordingly.

Autor dieses Artikels

Hubert Abt - Founder & CEO

EINBLICKE & RESSOURCEN

Siehe andere interessante Nachrichten

Sed ut perspiciatis unde omnis iste natus error sit voluptatem accusantium doloremque laudantium, totam rem aperiam.

Möchten Sie mehr erfahren?

Buchen Sie eine kostenlose Beratung mit Hubert!

Während des Anrufs werden wir den Prozess im Detail erklären und alle zusätzlichen Fragen beantworten, die Sie haben könnten.